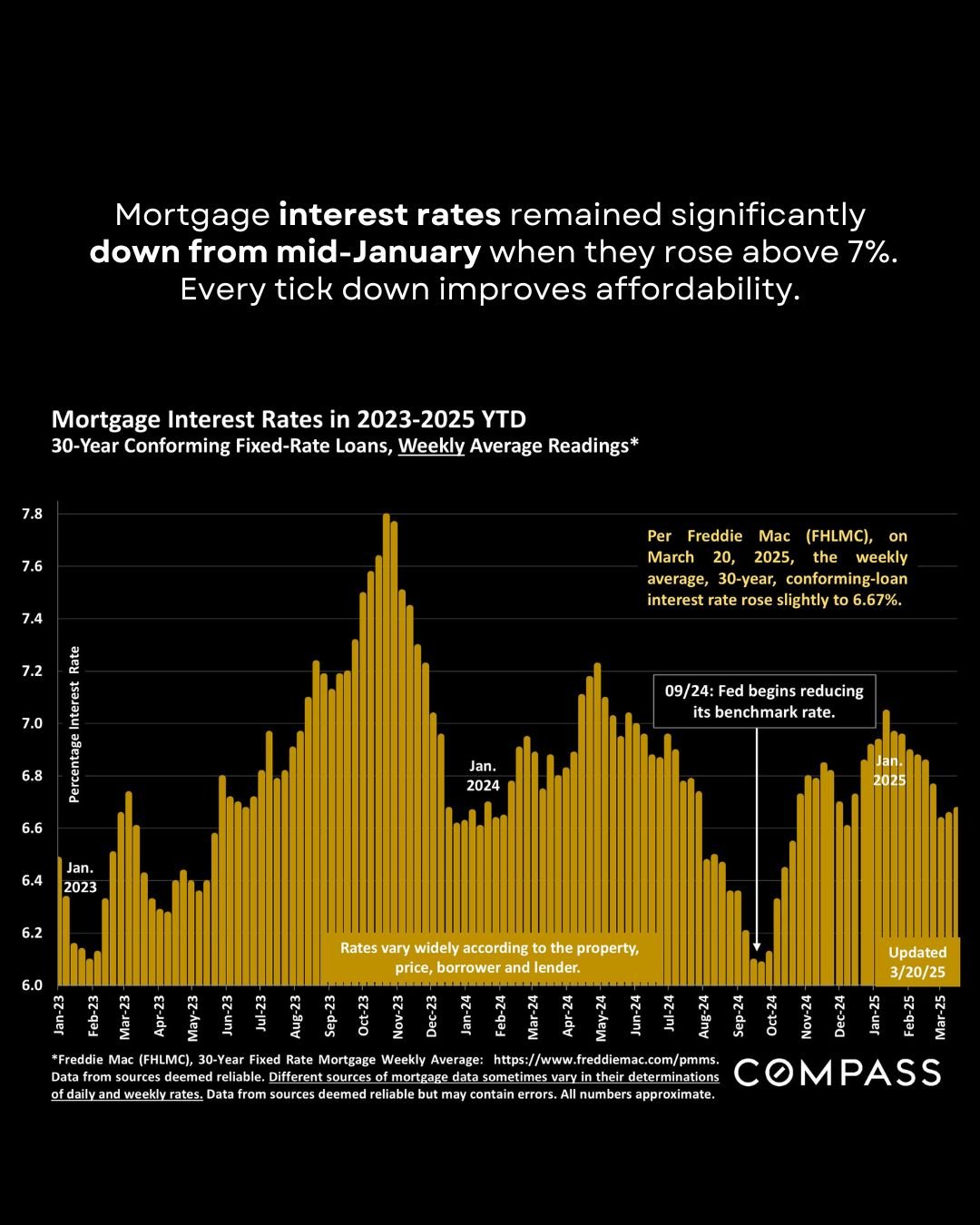

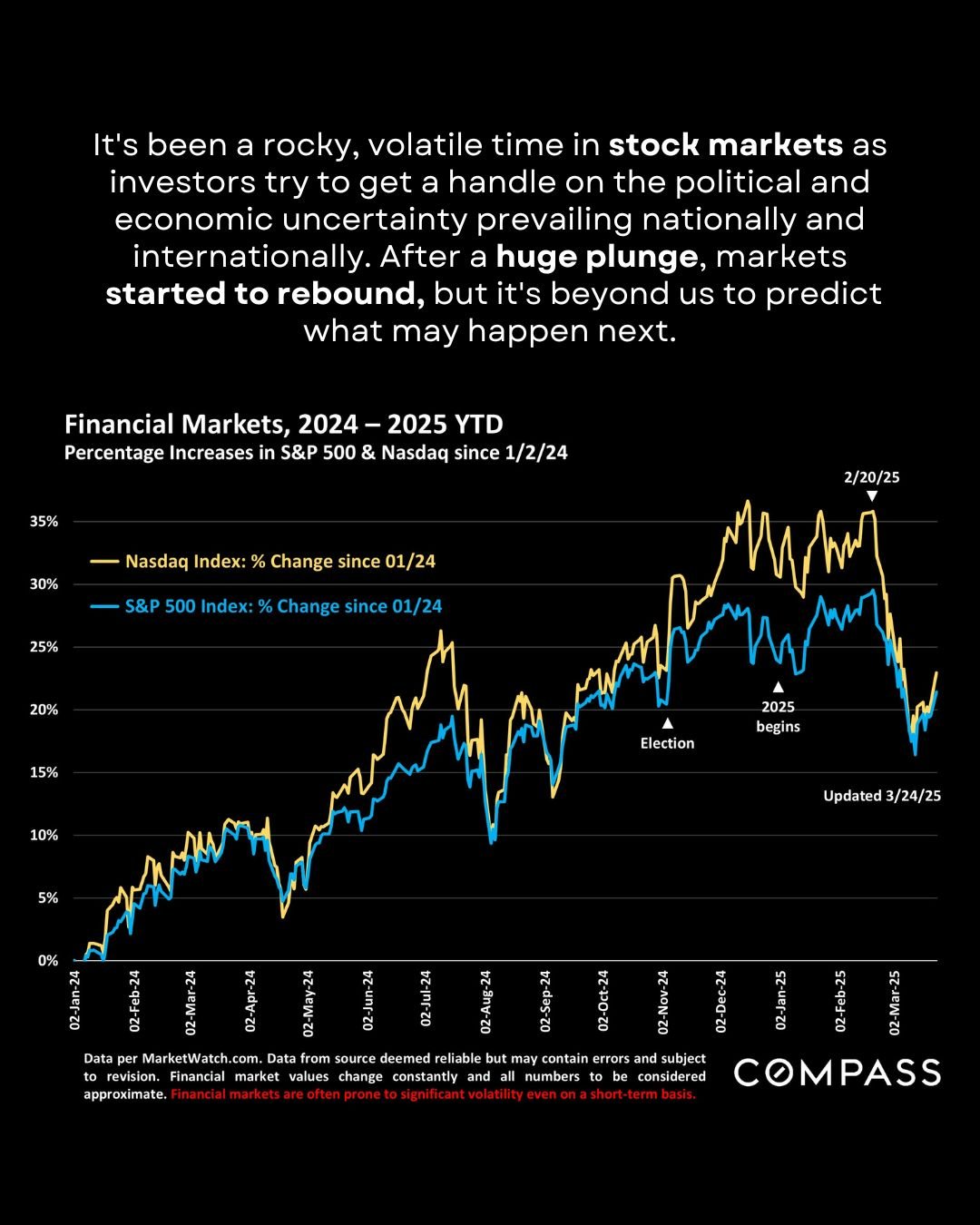

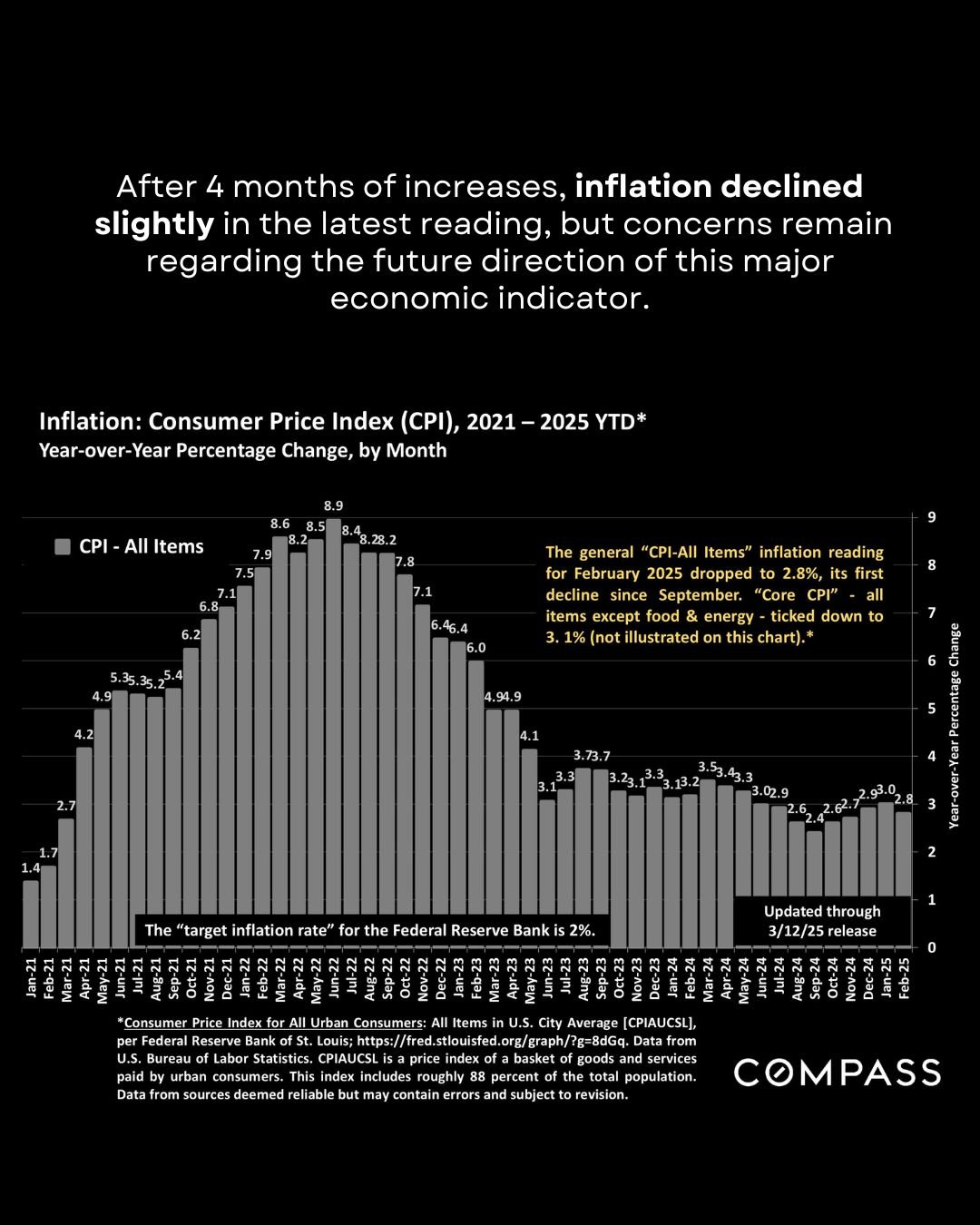

Inflation ticked down, the Fed again kept its benchmark rate unchanged, interest rates stayed well below 7%, and consumer confidence continued to fall across all population segments. Stock markets saw substantial declines, and then some recovery toward the end of the month. Generally, the broader market is more affected by interest rates and affordability, while the luxury market is influenced by the stock market and household wealth.

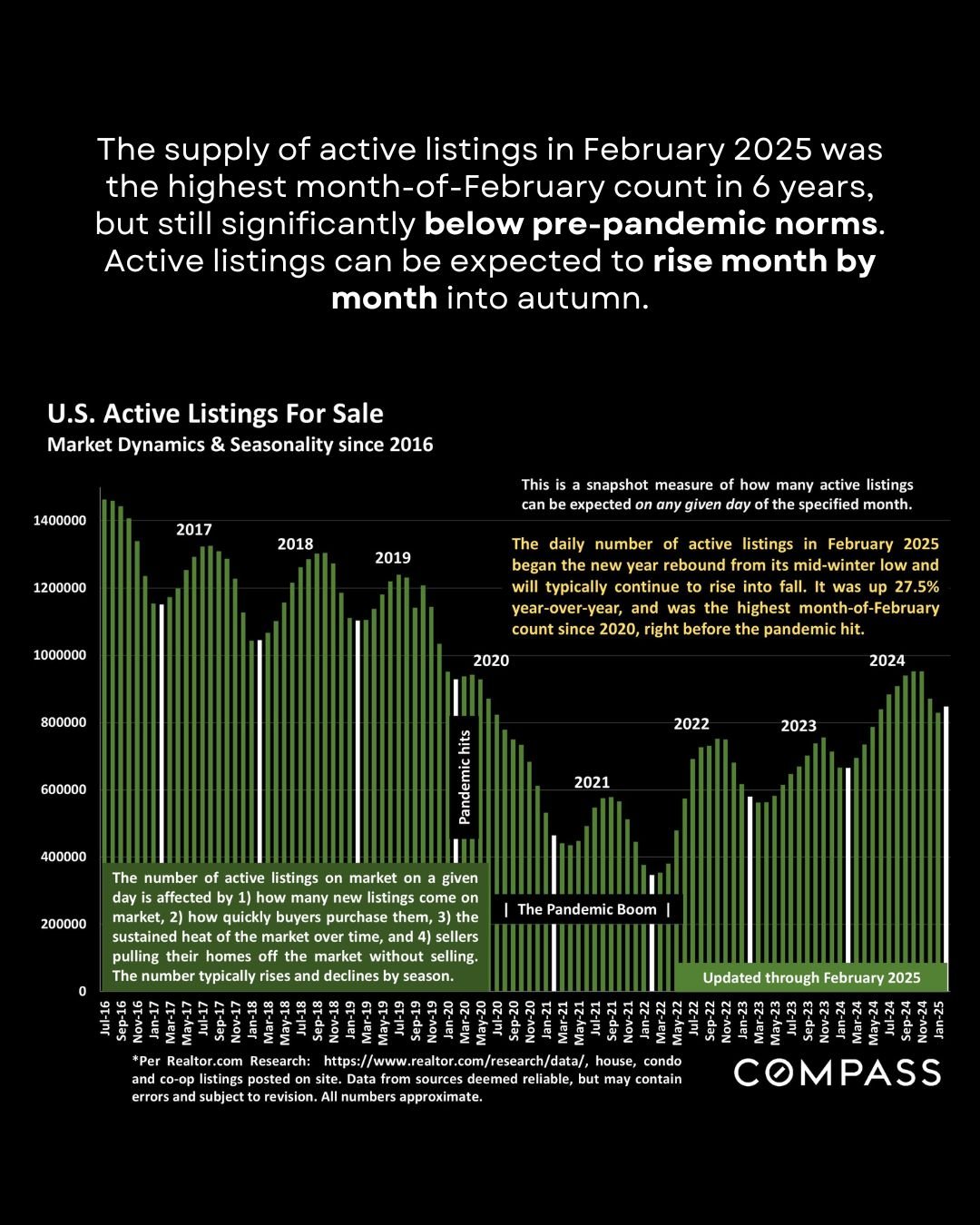

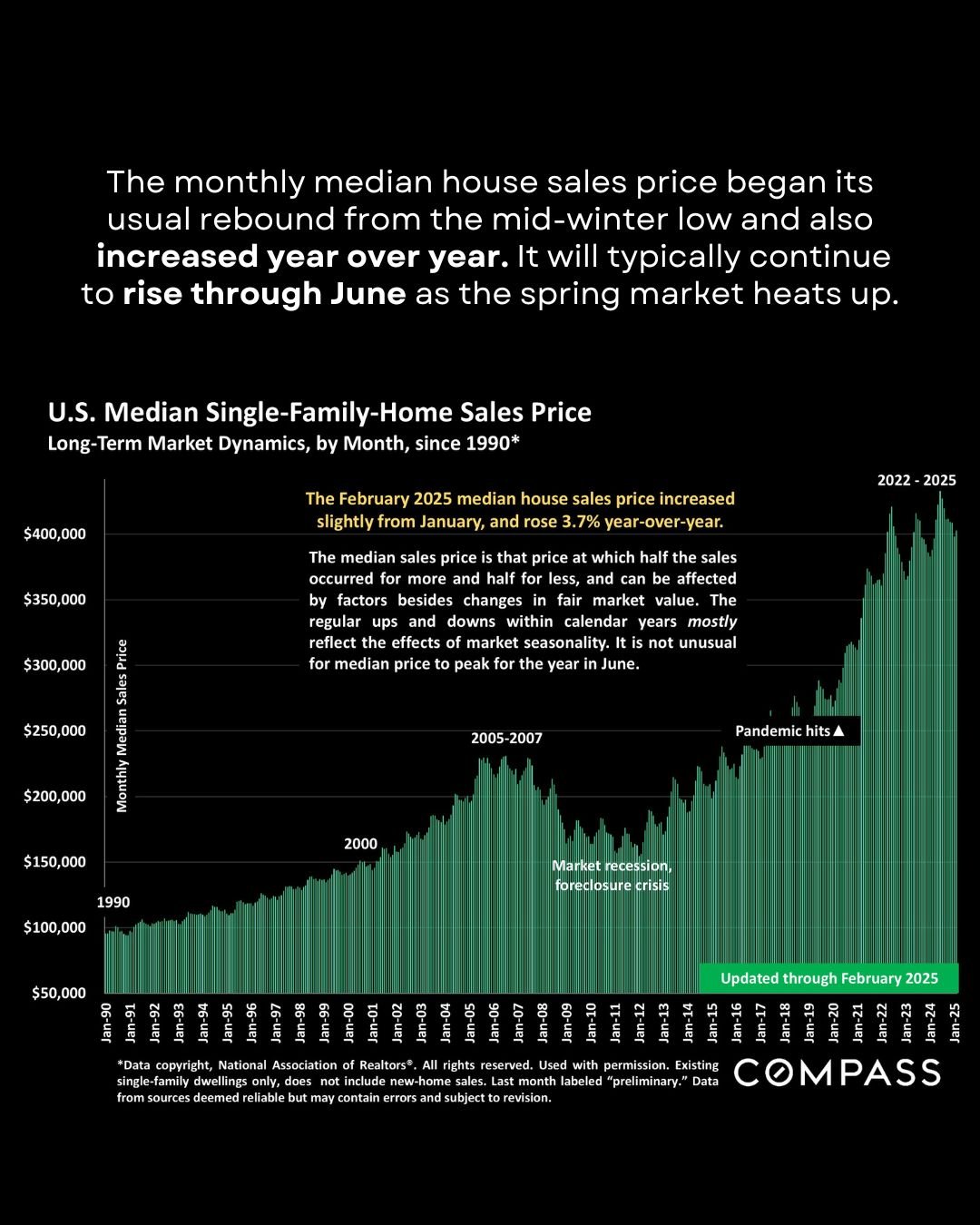

Year-over-year, monthly median home prices were up over 3%, 50% of homes sold in less than a month, and 21% closed for over asking price. All-cash sales rose to 32%, and first-time buyer sales rose to 31%. 24% of buyers waived their inspection and appraisal contingencies. The number of new listings rose 8% from January, and 4% YOY. It can be expected to climb through May or June.

Much of February still reflects the late-winter market; March is typically when the spring selling season really begins!